TXCRE Broker delivers a concierge-style commercial real estate experience that goes far beyond signing a lease. Instead of leaving clients to manage vendors, utilities, and move-in logistics alone, TXCRE handles the entire process from lease to lights-on.

Here's something most national CRE reports won't tell you: the Texas commercial real estate market isn't one market. It's four. And right now, each of those four metros -- DFW, Houston, Austin, and San Antonio -- is telling a completely different story.

If you're searching for office space, the conditions in Austin are practically the opposite of what you'd find in DFW. If you're looking for industrial space, Houston is operating in a different universe than San Antonio. If you own retail property, where your building sits changes everything about how quickly it leases, what you'll get for it, and who's interested.

This breakdown is written for business owners and property owners who are making real decisions -- not for people who want a vague overview of market sentiment. You'll get submarket-level specifics, honest assessments of where opportunities actually exist right now, and practical guidance on what these conditions mean before you sign anything or list anything.

It's worth taking a second to understand why Texas CRE behaves differently than most other states, because it shapes every submarket trend you're about to read.

Texas added more people than any other state for the third consecutive year, with the Dallas-Fort Worth and Houston metros each absorbing hundreds of thousands of new residents. Austin continues to grow despite its tech sector recalibration. San Antonio is expanding steadily and quietly. This isn't speculative growth driven by low interest rates -- it's structural. People and companies are genuinely relocating here, and they need space to operate.

That population and business migration create a floor underneath Texas commercial real estate that most markets don't have. Retail needs customers, customers come from residents, and Texas keeps adding both. Industrial needs supply chains and labor pools, and Texas has them. Office demand follows corporate relocations, and those relocations haven't stopped.

Now here's where it gets nuanced: population growth doesn't mean every property type in every submarket is thriving. The market has bifurcated sharply. The best corridors and the best product are being absorbed quickly. Secondary locations and dated assets are struggling. The gap between the two has widened more in the past 18 months than at any point in the past decade.

That gap is where the real decisions live. So let's break down each market.

If you want to understand what a genuinely healthy commercial real estate market looks like, start with Dallas-Fort Worth. Over 8 million people. Over 100,000 net new residents annually. A business-friendly regulatory environment that's attracted corporate relocations from California, Illinois, New York, and virtually every other high-cost state. And a commercial real estate market that's been absorbing space at a pace that has kept developers and landlords busy for years.

But not every corner of DFW is equal. Here's what's actually happening inside the market.

DFW retail vacancy sits at approximately 4.8 percent -- one of the tightest rates nationally for a market of this size. That number doesn't mean every retail space is in demand, but it does mean that well-located, right-sized spaces in strong corridors are moving fast.

The corridors generating the most leasing activity right now:

What's leasing quickly across DFW: second-gen restaurant space, medical retail, fitness and wellness studios, veterinary and pet services, and neighborhood-serving concepts in dense suburban nodes with strong anchor tenants.

What's sitting: large-format retail above 10,000 square feet in secondary corridors, Class C strip centers without recent renovation, and free-standing retail in locations where the surrounding population density hasn't caught up to the original development thesis.

The headline office vacancy number in DFW -- approximately 19 percent -- sounds alarming. It's not the full story.

What's actually happening is a bifurcation that's become more dramatic with every passing quarter. Class A office space in Uptown Dallas, Legacy/Frisco, the Dallas Arts District, and the Plano/Allen/McKinney corridor is absorbing steadily. Companies that are bringing employees back to the office want environments that make people want to come back -- modern amenities, walkable surroundings, good parking, and genuine quality. Those buildings are full.

Class B and Class C office in suburban parks built 20+ years ago, with dated common areas, aging HVAC systems, and limited walkable amenities? That's where the vacancy concentration lives. And those buildings aren't recovering without significant capital investment.

For tenants, this market is creating a real opportunity. Landlords of Class A buildings are competing for quality tenants by offering:

If your business needs office space in DFW and you've been hesitating, the window to capture these conditions is real. The best assets won't stay this generous as absorption continues.

For office building owners: the market is telling you something clearly. Tenants are making choices based on quality, amenities, and location specificity. A generic listing with no positioning strategy isn't going to move.

Owners who are investing in renovation, improving common areas, and working with brokers who are actively reaching out to tenant reps -- not just waiting for inbound inquiries -- are the ones filling space.

Houston's commercial real estate market is driven by two forces: an industrial sector that's structurally stronger than almost any other U.S. metro, and a suburban retail opportunity that most tenants outside the market haven't figured out yet.

The Port of Houston is the largest U.S. seaport by foreign tonnage. That's not a marketing line -- it's a structural economic fact that shapes how industrial real estate in this market performs. Supply chains route through Houston. Distribution centers locate near Houston. Manufacturing facilities want access to Houston's port, workforce, and rail infrastructure.

Industrial vacancy in Houston sits at approximately 6.1 percent with healthy absorption continuing. The submarkets generating the most deal activity:

What's leasing well: warehouse and distribution facilities with dock-high loading (multiple doors preferred), clear heights of 24 feet or above, adequate electrical capacity (at least 480V/3-phase for most modern industrial users), and yard space for trailer storage or outdoor operations.

What tenants consistently get wrong in Houston industrial: focusing on square footage without confirming power capacity and clear height first. A 15,000 square foot building with 16-foot clear heights and single-phase power is fundamentally incompatible with most distribution and manufacturing operations. Know your specs before you start touring, or you'll waste weeks on spaces that can't actually work for your business.

While DFW's suburban retail corridors are getting competitive, Houston's suburban ring is posting vacancy numbers below 5 percent in several key nodes with far less tenant competition. Here's why this matters:

Markets like Katy, Sugar Land, Pearland, The Woodlands, and League City are experiencing population-driven retail demand that genuinely outpaces new supply. These aren't markets where development has overbuilt -- they're markets where the residential growth has been so consistent that retail inventory is being absorbed as fast as it's delivered.

For tenants considering Houston: if you're flexible on location and your business model works in a suburban trade area with strong household incomes and consistent foot traffic, the suburban Houston ring gives you more viable options at better rates than equivalent positions in DFW's tightest corridors. The competitive dynamic simply hasn't caught up yet.

For property owners in these submarkets, well-located, well-maintained retail in these nodes has real pricing power right now. Occupancy is strong, tenant demand is genuine, and buyers looking at income-producing retail assets are actively evaluating Houston suburban product.

Austin's commercial market has been through a lot in the past three years, and the current conditions create one of the most interesting tenant opportunities in Texas right now -- but you have to understand what's actually happening to take advantage of it.

Office vacancy in Austin sits at approximately 22 percent -- the highest of the four major Texas markets. This is a direct result of the post-pandemic tech sector contraction. Companies that signed large office leases in 2020 and 2021 while riding the remote work boom subsequently downsized, consolidated, or departed. The wave of sublease availability that followed pushed vacancy to levels Austin hadn't seen in years.

Here's what the vacancy number means in practical terms:

Landlord motivation is at its highest in a decade. Buildings that were commanding $45-$55 per square foot in 2022 are having real conversations at $35-$42 with aggressive concession packages. TI allowances that were $50-$65/sf two years ago are now $70-$100/sf in competitive situations. Free rent periods of 4-8 months are being offered on 3-5 year leases. And term flexibility that simply wasn't available during the post-pandemic boom is now on the table.

The catch: landlords are motivated, not desperate. They're still evaluating tenants carefully. Companies with clean financials, a clear space plan, and a broker who knows which buildings are actively dealing -- versus which ones are holding firm on pricing -- are the ones capturing the best packages.

Don't let Austin's office narrative bleed into your assessment of retail. The two are telling very different stories.

South Congress, East Cesar Chavez, the Domain's retail corridors, and the Barton Creek/Southwest Austin nodes are performing well. Austin has a consumer culture -- particularly in its core neighborhoods -- that continues to support independent retail, experience-driven food and beverage, and local brands with strong community identity.

Where Austin retail gets hard: suburban nodes where development has outpaced population density, and generic strip retail that lacks differentiation or anchor draw. Those spaces are sitting longer and requiring more landlord flexibility to fill.

San Antonio doesn't generate the CRE headlines that DFW and Austin do. And that's precisely what makes it one of the best-positioned markets in Texas for tenants who are paying attention.

Retail vacancy: approximately 5.2 percent. Industrial demand: accelerating. Population growth: consistent and sustained, driven by a uniquely diversified economic base -- military, healthcare, hospitality, manufacturing, and now a growing technology and cybersecurity sector tied to Fort Sam Houston and Lackland Air Force Base.

San Antonio doesn't have Austin's volatility or DFW's intensity. What it has is steady, predictable demand across multiple property types, submarkets that are absorbing without the competitive pressure you'd face in North Texas, and base rents that remain meaningfully below comparable positions in the other major Texas markets.

San Antonio sits 150 miles from Laredo, the largest land port of entry on the U.S.-Mexico border. That geography matters enormously for companies with cross-border supply chains, and it's driving consistent industrial demand that many national tenants overlook when they're focused on DFW and Houston.

Industrial vacancy in San Antonio is in the range of 7-8 percent with absorption trending in the right direction. What makes San Antonio compelling for industrial tenants isn't just the availability of space -- it's the pricing. You can secure functional warehouse and distribution space here at rates 15-25 percent below comparable Houston or DFW product. For businesses where occupancy cost is a major factor in margin, that differential compounds over a 5-year lease term into a genuinely significant number.

Every market is offering something different right now, and the tenants winning the best deals are the ones who walk in understanding the environment before they start touring.

Here's the practical translation by market:

The single biggest mistake owners are making in the current Texas market is treating a strong market as a reason not to work the asset.

Here's the reality: there's a strong market for the right product in the right location. There's a stagnant market for everything else. And the gap between those two groups has widened dramatically.

If you're in the 'strong' category -- well-located, quality product, correctly priced -- a few things will determine whether you capture the demand that exists:

If you're in the 'struggling' category -- dated product, secondary location, or simply not differentiated from what's available at a lower price -- the market is giving you clear feedback. The options are reposition (invest in the asset), reprice (accept where market demand actually is), or wait out a market that isn't going to drift in your direction on its own.

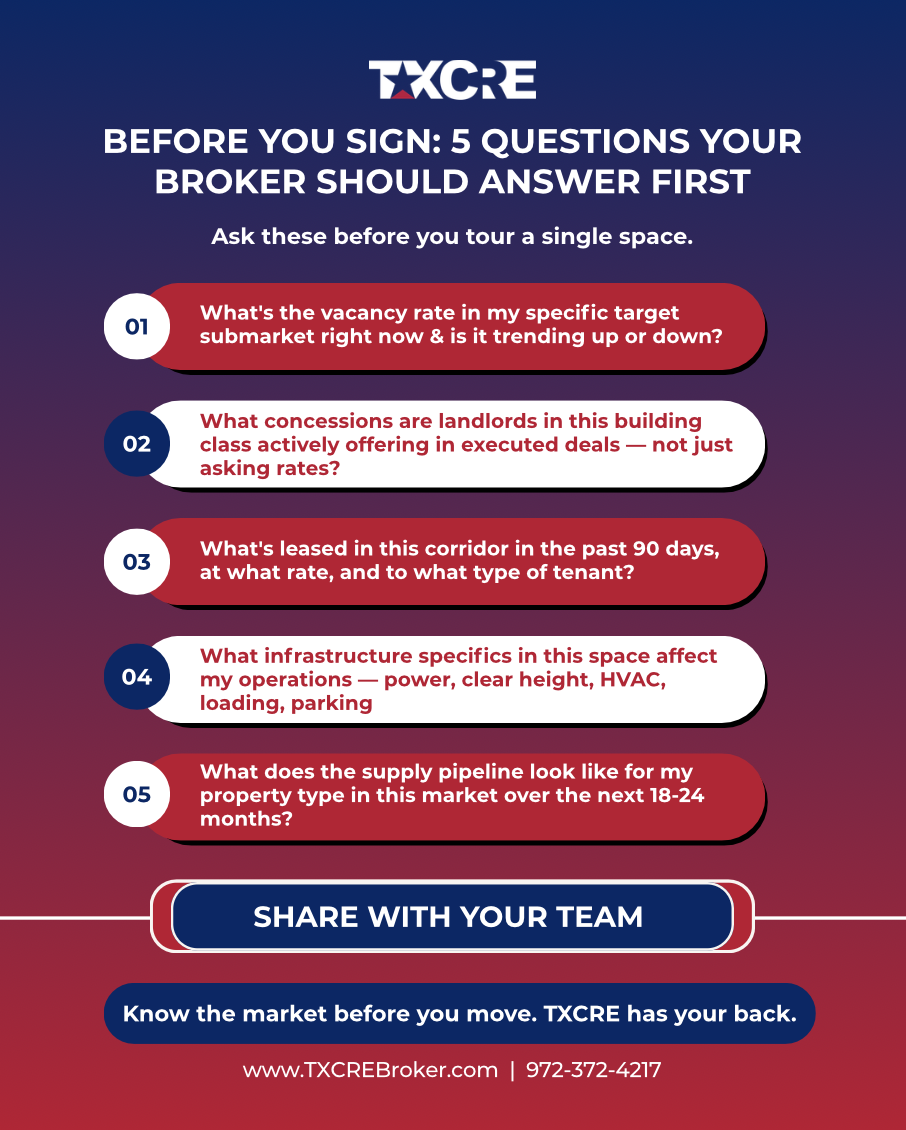

Whether you're a tenant about to tour space or an owner about to list, these questions will tell you immediately whether you're working with someone who actually knows the Texas market:

TXCRE operates across all four Texas markets -- DFW, Houston, Austin, and San Antonio -- every week. We're in these submarkets, on these deals, and in these conversations. The intelligence we share here comes from that active presence, not from third-party reports.

If you're a tenant trying to figure out where to search, what you should be paying, and which landlords are actually dealing, we'll give you that read before you tour a single space. If you're a property owner trying to understand where your asset sits in the current market and what it'll take to lease or sell it, we'll give you a straight answer.

No pitch. No pressure. Just an honest conversation about what the market looks like right now.

Call 972-372-4217 or visit txcrebroker.com/contact-us to schedule your complimentary market consultation.

Q: What's the current commercial real estate vacancy rate in DFW?

A: DFW retail vacancy is approximately 4.8 percent, among the tightest nationally for a market its size. Office vacancy is approximately 19 percent metro-wide, but Class A product in Uptown, Legacy, and Frisco is absorbing well. The metro average obscures a sharp bifurcation between high-quality assets and everything else.

Q: Is Houston industrial real estate still a good market for tenants?

A: It's a strong market with real demand, which means tenants shouldn't expect to find abundant availability at soft pricing. Industrial vacancy sits around 6.1 percent with consistent absorption. Well-configured product with dock-high loading, adequate power, and modern clear heights is leasing at a premium. Come in with defined specs and a broker who knows the submarkets or you'll spend weeks on properties that don't actually fit.

Q: Is Austin office space a good deal for tenants right now?

A: It's one of the best office tenant markets in Texas right now. Vacancy near 22 percent means landlords are motivated. TI packages, free rent, below-market base rents, and flexible terms are all negotiable in ways they weren't 2-3 years ago. But you need representation to know which buildings are genuinely open to dealing and which ones are just testing the market.

Q: Why should I consider San Antonio for commercial space when DFW gets all the attention?

A: Because less competition and lower pricing with solid demand fundamentals is the definition of an opportunity. San Antonio's retail vacancy is around 5.2 percent, its industrial market is absorbing, and base rents are 15-25 percent below comparable DFW and Houston positions. The metro's population growth is consistent, its economic base is diversified, and the pricing hasn't yet caught up to where fundamentals suggest it should be. That gap is what makes it worth serious consideration.

Q: What property types are performing best across Texas commercial real estate right now?

A: Industrial is the strongest performer statewide, particularly in Houston and DFW. Retail in well-located, high-income suburban corridors is absorbing well. Medical office is in consistently high demand across all four markets, with limited quality supply. Class A office in the right submarkets is moving. Class B/C office in generic suburban parks is the biggest challenge across all four metros.

Q: Does TXCRE work with both tenants and property owners?

A: Yes. TXCRE provides tenant representation and landlord leasing/sales services across DFW, Houston, Austin, and San Antonio. We work across all six major property types: retail, office, industrial, medical, flex, and multifamily. Our market intelligence comes from being active on both sides of transactions, which means we understand the market from the perspective of everyone at the table.

TXCRE Broker delivers a concierge-style commercial real estate experience that goes far beyond signing a lease. Instead of leaving clients to manage vendors, utilities, and move-in logistics alone, TXCRE handles the entire process from lease to lights-on.

Vacancy drains revenue and weakens leverage — but it doesn’t have to linger. With the right exposure, disciplined follow-up, and clear communication, commercial space in Texas can lease faster and more predictably. TXCRE Broker helps landlords reduce downtime through proactive strategy, professional execution, and responsiveness that keeps deals moving.